UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

[X]

|

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

For the fiscal year ended September 30, 2014.

|

[ ]

|

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

For the transition period from ______________ to _______________.

Commission File Number 0-16106

CLEARFIELD, INC.

(Exact Name of Registrant as Specified in its Charter)

|

Minnesota

|

41-1347235

|

|

(State of incorporation)

|

(I.R.S. Employer Identification No.)

|

|

5480 Nathan Lane North,

Suite 120

Plymouth, Minnesota 55442

|

(763) 476-6866

|

|

(Address of principal executive office)

|

Registrant’s telephone number, including area code

|

Securities registered pursuant to Section 12(b) of the Act:

|

(Title of class)

|

(Name of exchange on which registered)

|

|

Common Stock, par value $.01 per share

|

The NASDAQ Stock Market LLC

|

|

(Including Series B Junior Participating Preferred Share Purchase Rights)

|

|

Securities registered pursuant to Section 12(g) of the Act:

NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

[ ] YES [X] NO

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

[ ] YES [X] NO

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

[X] YES [ ] NO

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

[X] YES [ ] NO

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

[X] YES [ ] NO

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company as defined in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] Accelerated filer [X] Non-accelerated filer [ ] Smaller Reporting Company [ ]

Indicate whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

[ ] YES [X] NO

The aggregate market value of the voting and non-voting equity held by non-affiliates of the registrant, as of the last business day of the registrant’s most recently completed second fiscal quarter computed by reference to the price at which the common equity was last sold was approximately $255,722,720.

The number of shares of common stock outstanding as of November 15, 2014 was 13,746,164.

Documents Incorporated by Reference:

Portions of our proxy statement for the 2015 Annual Meeting of Shareholders, to be filed within 120 days after the end of the fiscal year covered by this report, are incorporated by reference into Part III.

CLEARFIELD, INC.

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

Background

Clearfield, Inc. (“Clearfield” or the “Company”), formerly APA Enterprises, Inc., is a Minnesota corporation which was founded in 1979. Our corporate headquarters are located at 5480 Nathan Lane North, Suite 120, Plymouth, MN 55442, and our corporate website is www.clearfieldconnection.com. The information available on our website is not part of this Report. You can access, free of charge, our filings with the Securities and Exchange Commission, including our annual report on Form 10-K, our quarterly reports on Form 10-Q, current reports on Form 8-K and any other amendments to those reports, through the “About Clearfield” link at our website, or at the Commission’s website at www.sec.gov.

Description of Business

Clearfield, Inc. manufactures, markets and sells an end-to-end fiber management and enclosure platform that consolidates, distributes and protects fiber as it moves from the inside plant to the outside plant and all the way to the home, business and cell site. The Company has extended this product line with a fiber delivery platform of optical cable, connectors and microduct that delivers fiber to environments previously not economically or environmentally viable. The Company has successfully established itself as a value-added supplier to its target market of broadband service providers, including independent local exchange carriers (telephone), multiple service operators (cable), wireless service providers, non-traditional providers and municipal-owned utilities. Clearfield has expanded its product offerings and broadened its customer base during the last five years.

By aligning its in-house engineering and technical knowledge alongside its customers’ needs, the Company has been able to develop, customize and enhance products from design through production. Substantially all of the final build and assembly is completed at Clearfield’s plant in Plymouth, Minnesota with manufacturing support from a network of domestic and global manufacturing partners. Clearfield specializes in producing these products on both a quick-turn and scheduled delivery basis. The Company deploys a hybrid sales model with some sales made directly to the customer, some made through two-tier distribution partners and some sales through original equipment suppliers who private label its products.

Products

Clearview Cassette

The Clearview™ Cassette, a patented technology, is the main building block of the Company’s product platform. The value of the building block approach is that Clearfield is the only company to provide the needs of every leg of the telecommunications network with a single building block architecture, reducing the customers’ cost of deployment by reducing labor costs associated with training and reducing inventory carrying costs.

Clearview Classic and Clearview Blue: Clearview Classic and Clearview Blue, is a system of five parts that nest together in the cassette’s main housing to support a wide range of applications. Parts can be added or removed as needed to support the environment in which it is deployed. Clearview Blue, while fully compatible with Clearview Classic, is designed for the utmost in modularity and scalability. It builds upon the Clearview Classic by offering a smaller footprint and integrated slack storage and splicing functionality.

Clearview xPAK: Engineered to land small port count fiber terminations and optical components, the patented xPAK is shipped flat and unassembled. Following simple pictorial user instructions, a technician will assemble the device to match his field requirements at the installation site. Application environments include cell back-haul, business class service delivery, node segmentation, fiber exhaust scenarios, utility sub-stations or fiber-to-the-desk deployment.

Connectivity and Optical Components

The Clearview system consolidates, distributes and protects fibers as they move from the inside plant to the home and business. These fibers are either connectorized directly for cable-to-cable deployment or are connectorized onto optical components that may amplify or divide the signals they carry. We provide products that meet a customer’s cable-to-cable deployment or optical component needs.

Cable-to-Cable Deployment: Fiber Deep is a class of fiber assemblies that guarantees performance at .2dB insertion loss – fully half that of the industry standard. This metric extends the link loss budget effectively, extending the distance upon which fiber can be deployed. In addition, this 2dB improvement in optical budget reduces power consumption by 10%. The power savings, multiplied by even a small thousand home network, is a significant contribution to a community’s “go-green” efforts.

Optical Components: Clearfield packages optical components for signal coupling, splitting, termination, multiplexing, demultiplexing and attenuation for a seamless integration within its fiber management platform. This value-added packaging allows the customer to source from a single supplier and reduces space requirements. The products are built and tested to meet the strictest industry standards ensuring customers trouble-free performance in extreme outside plant environments.

FieldSmart

Utilizing the Clearview Cassette and xPAK as building blocks, FieldSmart is a series of panels, cabinets, wall boxes and other enclosures that house the Clearview components to provide a consistent design from the inside plant of the telco’s “central office” or cable television’s “head-end”, all the way through the outside plant to the access network and through to the home. At each leg of the network, the FieldSmart platform delivers a modular and scalable architecture that allows the service provider to align their capital equipment expenditures alongside their subscriber revenues.

Inside Plant: The FieldSmart Fiber Crossover Distribution System (FxDS) and high density FieldSmart FxHD provides complete fiber management modularity and scalability across the fiber network. Using the Clearview building block approach, each fiber management element provides modularity of physical fiber protection in the environment in which it is placed. Easily configured for initial placement and scaling from 12-ports to a full rack of 1728-ports, the FieldSmart FxDS requires only four unique blocks to configure initial deployment. The user then places what is needed on the frame as subscriber take rates dictate. The FxHD is an integrated fiber management solution delivered via the Clearview Blue Cassette. With instant access to all cassettes, adapters, and jumpers, the frame is designed as a front access frame, meaning all installation is done from one side of the frame providing the option to reclaim the aisle space required for frame solutions that require rear access – and to use that space for other equipment or more frames. The FxHD can be placed against a wall, cage in data center co-location environments, or back to back.

Outside Plant: The FieldSmart Fiber Scalability Center (FSC) is a modular and scalable outside plant cabinet that allows rollout of Fiber-to-the-Premise services by communication service providers without a large initial expense. Each outside plant cabinet stores feeder and distribution splices, splitters, connectors and slack cable neatly and compactly, utilizing field-tested designs to maximize bend radius protection, connector access, ease of cable routing and physical protection, thereby minimizing the risk of fiber damage. The FSC product, with the Clearview cassette at its heart, has been designed to scale with the application environment as demand requires and to reduce service turn-up time for the end-user.

Access Network: FieldSmart Fiber Delivery Point (FDP) is a series of enclosure systems that incorporates the delivery of fiber connectivity to the neighborhood or business district in the most cost-effective footprint possible. This family of wall-mount enclosures provides 12 to 144 ports of connectivity for multi-dwelling unit fiber deployments, fiber demarcation, security systems (CCTV), telecommunications room needs and horizontal/intermediate cross-connects.

Access Network: FieldSmart Small Count Delivery (SCD) is a series of enclosure systems that are packaged to make landing small count fiber more cost-effective and efficient than previously thought possible. This family of wall-mount enclosures, panels and drop cable cases provide up to 12 ports of connectivity when fiber management is critical but high-count density is required. The FieldSmart SCD is targeted for application environments such as cell backhaul, business class service delivery, node segmentation, fiber exhaust in a field pedestal, sub-station turn-up or fiber-to-the-desk deployment.

FieldShield is a patent-pending fiber delivery method aimed at reducing the cost of broadband deployment. FieldShield takes industry standard glass and makes it easier and less expensive to install. FieldShield starts with a ruggedized microduct designed to support all aerial, direct bury, and inside plant “last mile” needs. Created from the most rugged HDPE polymers, FieldShield Microduct is strong enough to be placed using traditional methods of boring and plowing, leveraging existing conduit placement equipment, as well as newer, less disruptive technologies such as micro trenching or saw cutting.

FieldShield Pushable Fiber easily slips through the microduct's smooth inner wall. Utilizing bend-insensitive glass, FieldShield Pushable Fiber is available in a variety of fiber counts: 1 to 12 fibers in a 3mm jacket and up to 24 fibers in a 4mm jacket. Available in bulk reels or factory terminated, FieldShield offers total installation flexibility. FieldShield Pushable Fiber can be pushed by hand up to 100 feet or to distances up to 500 feet for direct bury applications and 300 feet for plenum and riser environments with the use of the FieldShield Assist Module, Clearfield’s cordless drill-driven machine. A factory pre-connectorized FieldShield Pushable Connector eliminates costly labor in the field and presents reliable, consistent and guaranteed performance along with lower installation costs. After being installed in the microduct, the slip-resistant protective housing is removed and the connector snaps together - all in seconds, providing a cost-effective, tech-friendly means of installing optical fiber without jeopardizing fiber protection.

The FieldShield Multiport SmarTerminal extends the reach of FieldShield optical fiber to the hardened connector marketplace. Teaming a FieldShield Pushable Connector with a field-installable, tool-less smart housing that provides a water tight seal decreases installation and maintenance time, while providing superior durability and reliability in the drop segment of the network. These new solutions, FieldShield Hardened Connectors and the FieldShield Multiport SmarTerminal, bring together the advantages of hardened connector technology with the ease of use and cost reductions associated with pushable fiber.

CraftSmart

CraftSmart is a full line of optical protection field enclosures, extending Clearfield presence in the fiber industry. The CraftSmart Fiber Protection Pedestals (FPP) and CraftSmart Fiber Protection Vaults (FPV) are integrated solutions, optimized to house FieldSmart products at the last mile access point of the network in above-grade or below-grade installations.

CraftSmart aims to optimize fiber protection and storage while ensuring industry standards. Utilizing methods of sealing and below-grade protection, along with Clearfield innovation, CraftSmart is a turn-key solution for the deployment of passive optics from the central office/head-end to the customer premise.

Cable Assemblies

Clearfield manufactures high quality fiber and copper assemblies with an industry-standard or customer-specified configuration. Industry-standard assemblies built include but are not limited to: single mode fiber, multimode fiber, multi-fiber, CATV node assembly, DS1 Telco, DS 3 (734/735) coax, Category 5e and 6, SCSI, Token Ring, and V.35. In addition, Clearfield’s engineering services team works alongside the engineering design departments of our OEM customers to design and manufacture custom solutions for both in-the-box as well as network connectivity assemblies specific to that customer’s product line.

Markets

FTTP

Fiber to the Premise (also called Fiber to the Home) is a means of delivering the highest possible level of bandwidth directly to the user. The Company’s sales and marketing efforts have principally been focused on the U.S., with investments in Canada and the Caribbean regions added in recent years.

FTTB

Fiber to the Business is the rapid expansion of fiber services, principally by multiple service (cable TV) operators to penetrate the business marketplace.

FTT-Cell site

Fiber to the Cell site is the trend in which wireless service providers are re-focusing their efforts from building towers for coverage to enhancing their coverage for bandwidth. Fiber is the medium of choice for their upgrade. Currently, a very small percentage of these cell sites are served by fiber.

DAS

A distributed-antenna system, or DAS, is a network of spatially separated antenna nodes connected to a common source via a transport medium that provides wireless service within a geographic area or structure. DAS antenna elevations are generally at or below the clutter level and node installations are compact. Fiber may be used to backhaul data from the antenna.

Build to Print

In addition to a proprietary product line designed for the broadband service provider marketplace, Clearfield provides contract manufacturing services for original equipment manufacturers requiring copper and fiber cable assemblies built to their specification.

Competition

Competitors to the FieldSmart product lines include, but are not limited to, Corning Cabling Systems, Inc., OFS (Furukawa Electric North America, Inc.), AFL Telecommunications (a subsidiary of Fujikura Ltd.), Fujikura Ltd., Alcatel, Inc., and TE Connectivity, Inc. (formerly Tyco Electronics). Competitors to the CraftSmart product line include Emerson Network Power, a subsidiary of Emerson Electric Co., and Charles Industries, Ltd. Competitors to FieldShield include Arnco Duraline and M2FX. Nearly all of these firms are substantially larger than Clearfield and as a result may be able to procure pricing for necessary components and labor at much lower prices. Clearfield believes that it has a competitive advantage with customers who can leverage the cost savings the Clearview Cassette can provide and those who require quick-turn, high-performance customized products, and that it is at competitive disadvantage with customers who principally seek large volume commodity products.

Sources of Materials and Outsourced Labor

Numerous purchased materials, components, and labor are used in the manufacturing of the Company’s products. Most of these are readily available from multiple suppliers. However, some components and outsourced labor are purchased from a single or a limited number of suppliers. The loss of access to some components and outsourced labor could have an adverse effect on our ability to deliver products on a timely basis and on our financial performance.

Major Customers and Financial Information about Geographic Areas

The following table summarizes customers comprising 10% or more of net sales for the years ended September 30, 2014, 2013, and 2012:

| |

|

Year Ended September 30,

|

|

| |

|

2014

|

|

|

2013

|

|

|

2012

|

|

|

Customer A

|

|

|

21 |

% |

|

|

23 |

% |

|

|

* |

|

|

Customer B

|

|

|

19 |

% |

|

|

19 |

% |

|

|

22 |

% |

* Less than 10%

As of September 30, 2014, Customer C accounted for 10% of accounts receivable. As of September 30, 2013, Customer A accounted for 57% of accounts receivable.

The Company allocates sales from external customers to geographic areas based on the location to which the product is transported. The following table presents our domestic and international sales for each of the last three fiscal years:

| |

|

Year Ended September 30,

|

|

| |

|

2014

|

|

|

2013

|

|

|

2012

|

|

|

United States

|

|

$ |

52,687,000 |

|

|

$ |

50,358,000 |

|

|

$ |

36,414,000 |

|

|

All Other Countries

|

|

|

5,358,000 |

|

|

|

2,995,000 |

|

|

|

1,060,000 |

|

|

Total Net Sales

|

|

$ |

58,045,000 |

|

|

$ |

53,353,000 |

|

|

$ |

37,474,000 |

|

Patents and Trademarks

As of September 30, 2014, we had four patents granted and four pending patent applications pending inside and outside the United States. We have also developed and are using trademarks and logos to market and promote our products, including Clearfield®, Clearview®, FieldSmart®, FieldShield®, and CraftSmart.®

Backlog

Backlog reflects purchase order commitments for our products received from customers that have yet to be fulfilled. Backlog orders are generally shipped within three months. The Company had a backlog of $3,340,000, $8,638,000, and $2,647,000 as of September 30, 2014, 2013, and 2012, respectively.

Seasonality

We are affected by the seasonal trends in the industries we serve. We typically experience sequentially lower sales in our first and second fiscal year quarters, primarily due to customer budget cycles, deployment schedules, some customer geographical concentrations as well as standard vacation and holiday calendars. Sales usually reach a seasonal peak in our third and fourth fiscal quarters.

Product Development

Product development for Clearfield’s product line program has been conducted internally. We believe that the communication industry environment is constantly evolving and our success depends on our ability to anticipate and respond to these changes. Our focus is to analyze the environment and technology and work to develop products that simplify our customers’ business by developing innovative high quality products utilizing modular design wherever possible. Research and development are reflected in Selling, General & Administrative expenses and are not material to the overall expense total.

Employees

As of September 30, 2014, the Company had 185 full-time employees. We also have several part-time employees and independent contractors. None of our employees are covered by any collective bargaining agreement. We believe our employee relations to be good.

Segment Reporting

The Company operates in a single reportable segment.

Our results of operations could be adversely affected now that the stimulus funds of the American Recovery and Reinvestment Act are fully allocated and projections are nearing completion.

The American Recovery and Reinvestment Act (the “ARRA”), widely known as the “Stimulus Bill,” was enacted in February 2009. The ARRA allocated $7.2 billion in grants, loans and loan guarantees for broadband/wireless initiatives for rural un-served and underserved geographies across the country, with these initiatives administered by several federal agencies. This funding is available to a wide variety of organizations, including our customers and prospective customers, to purchase and implement network infrastructure and services to improve broadband coverage. As part of the criteria established by the federal agencies administering these programs, the projects to be funded through the federal stimulus plan must be approved by the state or states in which the projects will be located.

All ARRA funding for these broadband/wireless initiatives was allocated to awarded applicants prior to the start of this fiscal year. The majority of these projects were nearing completion by the end of fiscal year 2013.

National Broadband Plan’s transitioning from the USF to the CAF program may cause our customers and prospective customers to delay or reduce purchases.

In October of 2011, the Federal Communications Commission approved the National Broadband Plan which called for the restructuring of the long-standing USF (Universal Service Fund). A key element of this program is the transition out of the USF program, which awards an operating subsidy to telecommunications companies providing service to high-cost serving areas, to the Connect America Fund (CAF) which would provide a capital expenditure subsidy for the build-out of the country’s broadband network. In addition, other universal service and inter-carrier compensation reforms scheduled to begin in the coming years will eliminate subsidies that carriers have traditionally relied upon to support service in high-cost, rural areas. Our customers or prospective customers may delay purchases until the financial impact to them from the transition to the CAF becomes clear. To the extent our customers or prospective customers receive reduced subsidies under the CAF, they may reduce the spending associated with their projects, delay projects, or not pursue projects. Any of these actions may result in reduced demand for our products with these customers or prospective customers.

A significant percentage of our sales in the last two fiscal years have been made to a small number of customers, and the loss of these major customers would adversely affect us.

In fiscal year 2014, Customers A and B comprised approximately 21% and 19%, respectively, of net sales. In fiscal year 2013, Customers A and B comprised approximately 23% and 19%, respectively, of total sales. Additionally, Customer B comprised approximately 22% of total sales for the fiscal year ended September 30, 2012. These customers purchase our products from time to time through purchase orders and we do not have any agreement that guarantees future purchases by any of these major customers. The loss of any one or more of these customers, the substantial reduction, delay or cancellation in orders from any such customer or our inability to collect the accounts receivable from these customers, could have a material adverse effect on our business, financial position and results of operations.

Intense competition in our industry may result in price reductions, lower gross profits and loss of market share.

Competition in the telecommunications equipment and services industry is intense. Our competitors may have or could develop or acquire marketing, financial, development and personnel resources that exceed ours. Our ability to compete successfully will depend on whether we can continue to advance the technology of our products and develop new products, the acceptance of our products among our customers and prospective customers and our ability to anticipate customer needs in product development, as well as the price, quality and reliability of our products, our delivery and service capabilities and our control of operating expenses.

We cannot assure you that we will be able to compete successfully against our current or future competitors. Increased competition from manufacturers of telecommunications equipment such as ours may result in price reductions, lower gross profit margins, and increased discounts to customers and loss of market share and could require increased spending by us on research and development, sales and marketing and customer support.

Our results of operations could be adversely affected by economic conditions and the effects of these conditions on our customers’ businesses.

Adverse changes in economic conditions, including the recent recession in the United States, have resulted and may continue to result in lower spending among our customers and contribute to decreased sales to our distributors and customers. Further, our business may be adversely affected by factors such as downturns in economic activity in specific geographic areas or in the telecommunications industry; social, political or labor conditions; or adverse changes in the availability and cost of capital, interest rates, tax rates, or regulations. These factors are beyond our control, but may result in decreases in spending among customers and softening demand for our products. Declines in demand for our products will adversely affect our sales. Further, challenging economic conditions also may impair the ability of our customers to pay for products and services they have purchased. As a result, our cash flow may be negatively impacted and our allowance for doubtful accounts and write-offs of accounts receivable may increase.

Our operating results may fluctuate significantly from quarter to quarter, which may make budgeting for expenses difficult and may negatively affect the market price of our common stock.

Because many purchases by customers of our products relate to a specific customer project, the short-term demand for our products can fluctuate significantly and our ability to forecast sales accurately from quarter to quarter is limited. This fluctuation can be further affected by the long sales cycles necessary to obtain contracts to supply equipment for these projects, the availability of capital to fund our customers’ projects, and the impact of the government regulation to encourage service to unserved or underserved communities, rural areas or other high cost areas on customer buying patterns. These long sales cycles may result in significant effort expended with no resulting sales or sales that are not made in the anticipated quarter. Demand for our projects will also depend upon the extent to which our customers and prospective customers initiate these projects and the extent to which we are selected to provide our equipment in these projects, neither of which can be assured. In addition, a sharp increase in demand could result in actual lead times longer than quoted, and a sharp decrease in demand could result in excess stock. These factors generally result in fluctuations, sometimes significant, in our operating results.

Other factors that may affect our quarterly operating results including:

|

·

|

the volume and timing of orders from and shipments to our customers;

|

|

·

|

work stoppages and other developments affecting the operations of our customers;

|

|

·

|

the timing of and our ability to obtain new customer contracts and the timing of revenue recognition;

|

|

·

|

the timing of new product and service announcements;

|

|

·

|

the availability of products and services;

|

|

·

|

market acceptance of new and enhanced versions of our products and services;

|

|

·

|

variations in the mix of products and services we sell;

|

|

·

|

the utilization of our production capacity and employees;

|

|

·

|

the availability and cost of key components of our products; and

|

|

·

|

changes in the valuation allowance relating to our deferred tax assets and the resulting income tax benefits or expenses.

|

Further, we budget our expenses based in part on expectations of future sales. If sales levels in a particular quarter are lower than expected, our operating results will be affected adversely.

Because of these factors, our quarterly operating results are difficult to predict and are likely to vary in the future. If our operating results are below financial analysts’ or investors’ expectations, the market price of our common stock may fall abruptly and significantly.

To compete effectively, we must continually improve existing products and introduce new products that achieve market acceptance.

The telecommunications equipment industry is characterized by rapid technological changes, evolving industry standards, changing market conditions and frequent new product and service introductions and enhancements. The introduction of products using new technologies or the adoption of new industry standards can make our existing products, or products under development, obsolete or unmarketable. In order to remain competitive and increase sales, we will need to anticipate and adapt to these rapidly changing technologies, enhance our existing products and introduce new products to address the changing demands of our customers.

Many of our competitors have greater engineering and product development resources than we have. Although we expect to continue to invest substantial resources in product development activities, our efforts to achieve and maintain profitability will require us to be selective and focused with our research and development expenditures. Further, our existing and development-stage products may become obsolete if our competitors introduce newer or more appealing technologies. If these technologies are patented or proprietary to our competitors, we may not be able to access these technologies.

If we fail to anticipate or respond in a cost-effective and timely manner to technological developments, changes in industry standards or customer requirements, or if we experience any significant delays in product development or introduction, our business, operating results and financial condition could be affected adversely.

We may face circumstances in the future that will result in impairment charges, including, but not limited to, significant goodwill impairment charges.

If the fair value of any of our long-lived assets decreases as a result of an economic slowdown, a downturn in the markets where we sell products and services or a downturn in our financial performance and/or future outlook, we may be required to record an impairment charge on such assets, including goodwill.

We are required to test intangible assets with indefinite life periods for potential impairment annually and on an interim basis if there are indicators of a potential impairment. We also are required to evaluate amortizable intangible assets and fixed assets for impairment if there are indicators of a possible impairment. One potential indicator of impairment is the value of our market capitalization compared to our net book value. Significant declines in our market capitalization could require us to record material goodwill and other impairment charges. Impairment charges could have a negative impact on our results of operations and financial position, as well as on the market price of our common stock.

We rely on single-source suppliers, which could cause delays, increases in costs or prevent us from completing customer orders, all of which could materially harm our business.

We assemble our products using materials and components supplied by various subcontractors and suppliers. We purchase critical components for our products, including injected molded parts and connectors from third parties, some of whom are single- or limited-source suppliers. If any of our suppliers are unable to ship critical components, we may be unable to manufacture and ship products to our distributors or customers. If the price of these components increases for any reason, or if these suppliers are unable or unwilling to deliver, we may have to find another source, which could result in interruptions, increased costs, delays, loss of sales and quality control problems.

Further, the costs to obtain certain raw materials and supplies are subject to price fluctuations, which may be substantial, because of global market demands. Many companies utilize the same raw materials and supplies in the production of their products as we use in our products. Companies with more resources than us may have a competitive advantage in obtaining raw materials and supplies due to greater purchasing power. Some raw materials or supplies may be subject to regulatory actions, which may affect available supplies. Furthermore, due to general economic conditions in the United States and globally, our suppliers may experience financial difficulties, which could result in increased delays, additional costs, or loss of a supplier.

The termination or interruption of any of these relationships, or the failure of these manufacturers or suppliers to supply components or raw materials to us on a timely basis or in sufficient quantities, likely would cause us to be unable to meet orders for our products and harm our reputation and our business. Identifying and qualifying alternative suppliers would take time, involve significant additional costs and may delay the production of our products. If we fail to forecast our manufacturing requirements accurately or fail to properly manage our inventory with our contract manufacturers, we could incur additional costs, experience manufacturing delays and lose sales. Further, if we obtain a new supplier or assemble our product using an alternative source of supply, we may need to conduct additional testing of our products to ensure the product meets our quality and performance standards. Any delays in delivery of our product to distributors or customers could be extended, and our costs associated with the change in product manufacturing could increase.

The failure of our third-party manufacturers to manufacture the products for us, and the failure of our suppliers of components and raw materials to supply us consistent with our requirements as to quality, quantity and timeliness could materially harm our business by causing delays, loss of sales, increases in costs and lower gross profit margins.

Our success depends upon adequate protection of our patent and intellectual property rights.

Our future success depends in part upon our proprietary technology. We attempt to protect our proprietary technology through patents, trademarks, copyrights and trade secrets. However, these legal means afford us only limited protection and may not adequately protect our rights or remedies to gain or keep any advantages we may have over our competitors. Accordingly, we cannot predict whether these protections will be adequate, or whether our competitors will develop similar technology independently, without violating our proprietary rights.

Our competitors, who may have or could develop or acquire significant resources, may make substantial investments in competing technologies, or may apply for and obtain patents that will prevent, limit, or interfere with our ability to manufacture or market our products. Further, although we do not believe that any of our products infringe the rights of others, third parties may in the future claim our products infringe on their rights, and these third parties may assert infringement claims against us in the future.

We may litigate to enforce patents issued to us and to defend against claimed infringement of the rights of others or to determine the ownership, scope, or validity of our proprietary rights and the rights of others. Any claim of infringement against us could involve significant liabilities to third parties, could require us to seek licenses from third parties, and could prevent us from manufacturing, selling or using our products. The occurrence of this litigation, or the effect of an adverse determination in any of this type of litigation, could have a material adverse effect on our business, financial condition and results of operations.

Our failure to protect or enforce our intellectual property rights could have a material adverse effect on our business, results of operations and financial condition.

Further consolidation among our customers may result in the loss of some customers and may reduce sales during the pendency of business combinations and related integration activities.

We believe consolidation among our customers in the future will continue in order for them to increase market share and achieve greater economies of scale. Consolidation has impacted our business as our customers focus on completing business combinations and integrating their operations. In connection with this merger and acquisition activity, our customers may postpone or cancel orders for our product based on revised plans for technology or network expansion pending consolidation activity. Customers integrating large-scale acquisitions may also reduce their purchases of equipment during the integration period, or postpone or cancel orders.

The impact of significant mergers among our customers on our business is likely to be unclear until sometime after such transactions are completed. After a consolidation occurs, a customer may choose to reduce the number of vendors from which it purchases equipment and may choose one of our competitors as its preferred vendor. There can be no assurance that we will continue to supply equipment to the surviving communications service provider after a business combination is completed.

We are dependent on key personnel.

Our failure to attract and retain skilled personnel could hinder the management of our business, our research and development, our sales and marketing efforts and our manufacturing capabilities. Our future success depends to a significant degree upon the continued services of key senior management personnel, including Cheryl P. Beranek, our Chief Executive Officer and John P. Hill, our Chief Operating Officer. We have employment agreements with Ms. Beranek and Mr. Hill that provide that if we terminate the employment of either executive without cause or if the executive terminates her or his employment for good reason, we would be required to make specified payments to them as described in their employment agreements. We have key person life insurance on Ms. Beranek and Mr. Hill. Further, our future success also depends on our continuing ability to attract, retain and motivate highly qualified managerial, technical and sales personnel. Our inability to retain or attract qualified personnel could have a significant negative effect and thereby materially harm our business and financial condition.

Product defects or the failure of our products to meet specifications could cause us to lose customers and sales or to incur unexpected expenses.

If our products do not meet our customers’ performance requirements, our customer relationships may suffer. Also, our products may contain defects or fail to meet product specifications. Any failure or poor performance of our products could result in:

|

·

|

lack of or delayed market acceptance of our products;

|

|

·

|

delayed product shipments;

|

|

·

|

unexpected expenses and diversion of resources to replace defective products or identify and correct the source of errors;

|

|

·

|

damage to our reputation and our customer relationships;

|

|

·

|

delayed recognition of sales or reduced sales; and

|

|

·

|

product liability claims or other claims for damages that may be caused by any product defects or performance failures.

|

Our products are often critical to the performance of telecommunications systems. Many of our supply agreements contain limited warranty provisions. If these contractual limitations are unenforceable in a particular jurisdiction or if we are exposed to product liability claims that are not covered by insurance, a claim could harm our business.

Our stock price has been volatile historically and may continue to be volatile. The price of our common stock may fluctuate significantly.

The trading price of our common stock has been and may continue to be subject to wide fluctuations. Our stock price may fluctuate in response to a number of events and factors, such as quarterly variations in operating results, announcements of technological innovations or new products by us or our competitors, changes in financial estimates and recommendations by securities analysts, the operating and stock price performance of other companies that investors may deem comparable to us, and new reports relating to trends in our markets or general economic conditions.

In addition, the stock market is subject to price and volume fluctuations that affect the market prices for companies in general, and small-capitalization, high-technology companies like us in particular. These broad market and industry fluctuations may adversely affect the price of our common stock, regardless of our operating performance. Further, any failure by us to meet or exceed the expectations of financial analysts or investors is likely to cause a decline in our common stock price. Further, recent economic conditions have resulted in significant fluctuations in stock prices for many companies, including Clearfield. We cannot predict when the stock markets and the market for our common stock may stabilize. In addition, although our common stock is listed on the NASDAQ Stock Market, our common stock has at times experienced low trading volume in our past. Limited trading volume subjects our common stock to greater price volatility and may make it difficult for our shareholders to sell shares at an attractive price.

Future sales of shares of our common stock in the public market may negatively affect our stock price.

Future sales of our common stock, or the perception that these sales could occur, could have a significant negative effect on the market price of our common stock. In addition, upon exercise of outstanding options, the number of shares outstanding of our common stock could increase substantially. This increase, in turn, could dilute future earnings per share, if any, and could depress the market value of our common stock. Dilution and potential dilution, the availability of a large amount of shares for sale, and the possibility of additional issuances and sales of our common stock may negatively affect both the trading price of our common stock and the liquidity of our common stock.

Anti-takeover provisions in our organizational documents, Minnesota law and other agreements could prevent or delay a change in control of our company.

Certain provisions of our articles of incorporation and bylaws, Minnesota law and other agreements may make it more difficult for a third-party to acquire, or discourage a third-party from attempting to acquire, control of our company, including:

|

·

|

the provisions of our bylaws setting forth the advance notice and information requirements for shareholder proposals, including nominees for directors, to be considered properly brought before shareholders;

|

|

·

|

the right of our board of directors to establish more than one class or series of shares and to fix the relative rights and preferences of any such different classes or series;

|

|

·

|

the provisions of Minnesota law relating to business combinations and control share acquisitions; and

|

|

·

|

the provisions of our stock option plans allowing for the acceleration of vesting or payments of awards granted under the plans in the event of specified events that result in a “change in control” and provisions of agreements with certain of our executive officers requiring payments if their employment is terminated and there is a “change in control.”

|

These measures could discourage or prevent a takeover of us or changes in our management, even if an acquisition or such changes would be beneficial to our shareholders. This may have a negative effect on the price of our common stock.

Compliance with changing regulation of corporate governance and public disclosure may result in additional expenses.

Keeping abreast of, and in compliance with, changing laws, regulations and standards relating to corporate governance and public company disclosure requirements, including the Sarbanes-Oxley Act of 2002 and in particular Section 404 of that Act relating to management certification of internal controls, new disclosures relating to “conflict minerals”, the regulations of the Securities and Exchange Commission and the rules of the NASDAQ Stock Market have required an increased amount of management attention and external resources. We intend to invest all reasonably necessary resources to comply with evolving corporate governance and public disclosure standards, and this investment may result in increased general and administrative expenses and a diversion of management time and attention from revenue-generating activities to compliance activities.

We face risks associated with expanding our sales outside of the United States.

We believe that our future growth depends in part upon our ability to increase sales in international markets. These sales are subject to a variety of risks, including fluctuations in currency exchange rates, tariffs, import restrictions and other trade barriers, unexpected changes in regulatory requirements, longer accounts receivable payment cycles, potentially adverse tax consequences, and export license requirements. In addition, we are subject to the risks inherent in conducting business internationally, including political and economic instability and unexpected changes in diplomatic and trade relationships. Currency fluctuations may also increase the relative price of our product in international markets and thereby could also cause our products to become less affordable or less price competitive than those of international manufacturers. These risks associated with international operations may have a material adverse effect on our revenue from or costs associated with international sales.

|

|

UNRESOLVED STAFF COMMENTS

|

Not applicable.

Clearfield leases a 46,583 square foot facility at 5480 Nathan Lane North in Plymouth, Minnesota consisting of our corporate offices, manufacturing and warehouse space. The original lease commenced on July 1, 2006, with rent commencing on November 1, 2006. On March 28, 2013, the Company entered into an amendment to the original lease agreement that expanded its leased space as of April 1, 2013 by 16,845 square feet (which included approximately 9,561 square feet that was already being used by the Company pursuant to previous license agreements for this facility). This amendment also set the Company’s pro rata share of certain expenses for such additional leased space, set the base rent for the expanded lease space for the remainder of the term, and extended the term of the lease until February 28, 2015.

On September 9, 2014, the Company entered into a lease under which the Company will lease Suite 100 in the building commonly known as of 7050 Winnetka Avenue North, Brooklyn Park, Minnesota as its new headquarters. The lease term will commence on the later of January 1, 2015 or the date of substantial completion of build out of the leased premises. The Company estimates that it will incur approximately $2.1 million in capital expenditures relating to the build out of office, manufacturing, warehousing and distribution space within the 70,771 rentable square feet of the leased premises. The lease term is ten years and two months after the commencement date. However, upon proper notice and payment of a termination fee of approximately $214,000, the Company has a one-time option to terminate the lease effective as of the last day of the eighth year of the term after the Company commenced paying base rent. The lease also grants the Company a first right to lease contiguous space that becomes available in the building where the leased premises are located during the term of the lease.

There are no pending legal proceedings against or involving the Company for which the outcome is likely to have a material adverse effect upon its financial position or results of operations.

Not applicable.

|

|

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

Our common stock is traded on The NASDAQ Global Market system of The NASDAQ Stock Market LLC under the symbol “CLFD.”

The following table sets forth the quarterly high and low sales prices for our common stock for each quarter of the past two fiscal years.

|

Fiscal Year Ended September 30, 2014

|

|

High

|

|

|

Low

|

|

|

Quarter ended December 31, 2013

|

|

$ |

20.67 |

|

|

$ |

13.47 |

|

|

Quarter ended March 31, 2014

|

|

|

26.09 |

|

|

|

17.41 |

|

|

Quarter ended June 30, 2014

|

|

|

24.84 |

|

|

|

14.56 |

|

|

Quarter ended September 30, 2014

|

|

|

16.90 |

|

|

|

12.35 |

|

|

Fiscal Year Ended September 30, 2013

|

|

High

|

|

|

Low

|

|

|

Quarter ended December 31, 2012

|

|

$ |

5.35 |

|

|

$ |

4.16 |

|

|

Quarter ended March 31, 2013

|

|

|

6.01 |

|

|

|

4.84 |

|

|

Quarter ended June 30, 2013

|

|

|

12.90 |

|

|

|

5.76 |

|

|

Quarter ended September 30, 2013

|

|

|

14.76 |

|

|

|

9.74 |

|

The foregoing prices reflect inter-dealer prices, without dealer markup, markdown, or commissions and may not represent actual transactions.

Approximate Number of Holders of Common Stock

There were approximately 285 holders of record of our common stock as of September 30, 2014.

Dividends

We have never paid cash dividends on our common stock. We currently intend to retain any earnings for use in our operations and do not intend in the foreseeable future to pay cash dividends on our common stock.

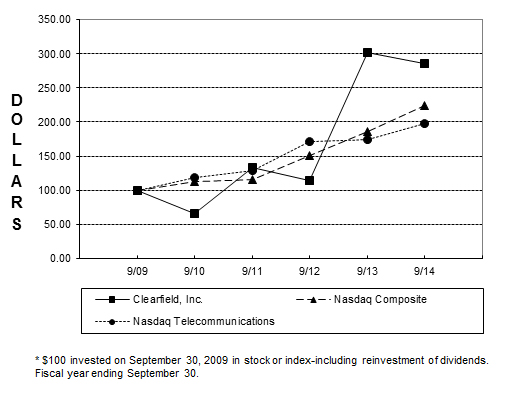

Stock Performance Graph

The information provided under this subsection shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the Exchange Act), or incorporated by reference into any filing of Clearfield, Inc. under the Securities Act of 1933, as amended, or the Exchange Act, except as shall be expressly set forth by specific reference in such filing.

The following graph shows a comparison of the 5-year cumulative total return on Clearfield, Inc.’s common stock relative to the NASDAQ Composite index, which the Company has selected as a broad market index, and the NASDAQ Telecommunications index, which the Company has selected as a published industry index. The graph assumes an investment of $100 (with reinvestment of all dividends) is made in the Company’s common stock and in each index on September 30, 2009 and its relative performance is tracked through September 30, 2014. The returns shown are based on historical results and are not intended to suggest future performance.

COMPARISON OF 5-YEAR CUMULATIVE TOTAL RETURN*

Among Clearfield, Inc., The NASDAQ Stock Market Composite Index

And The NASDAQ Telecommunications Index

Equity Compensation Plan Information

The following table describes shares of our common stock that are available on September 30, 2014 for purchase under outstanding stock-based awards, or reserved for issuance under stock-based awards or other rights that may be granted in the future, under our equity compensation plans:

|

Plan Category

|

|

Number of

securities to be

issued upon

exercise of

outstanding

options, warrants

and rights

|

|

|

Weighted-

average exercise

price of

outstanding

options, warrants

and rights

|

|

|

Number of

securities

remaining available

for future issuance

under equity

compensation plans

(excluding those

reflected in first

column)

|

|

|

Equity compensation plans approved by security holders

|

|

|

|

|

|

|

|

|

|

|

2007 Stock Compensation Plan

|

|

|

365,551 |

|

|

$ |

5.01 |

|

|

|

343,714 |

|

|

Stock Option Plan for Non- Employee Directors

|

|

|

7,500 |

|

|

|

1.16 |

|

|

|

- |

|

|

Total

|

|

|

373,051 |

|

|

$ |

4.93 |

|

|

|

343,714 |

|

All outstanding equity awards have been granted pursuant to shareholder-approved plans. In addition to options, shares may be issued in the form of restricted stock awards and other stock-based awards.

Issuer Repurchases

The Company repurchased a total of 16,560 shares of our common stock during the fourth quarter of fiscal year 2014 in connection with payment of taxes upon the vesting of restricted stock previously issued to employees.

The following table presents the total number of shares repurchased during the fourth quarter of fiscal 2014 by month and the average price paid per share:

|

Period

|

|

Total number of

shares withheld

|

|

|

Average price

paid per share

|

|

|

July 1-31, 2014

|

|

|

- |

|

|

$ |

- |

|

|

August 1-31, 2014

|

|

|

16,560 |

|

|

|

13.61 |

|

|

September 1-30, 2014

|

|

|

- |

|

|

|

- |

|

|

Total

|

|

|

16,560 |

|

|

$ |

13.61 |

|

On November 13, 2014, the Company announced that its board of directors had approved a stock repurchase program under which it will begin purchasing up to $8 million of its outstanding shares of common stock.

The program does not obligate Clearfield to repurchase any particular amount of common stock during any period. The repurchase will be funded by cash on hand. The repurchase program is expected to continue indefinitely until the maximum dollar amount of shares has been repurchased or until the repurchase program is earlier modified, suspended or terminated by the board of directors.

The following selected financial data has been derived from our financial statements and should be read in conjunction with the Financial Statements and related notes thereto set forth in Item 8 and with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in Item 7 of this Annual Report on Form 10-K.

| |

|

Year Ended September 30

|

|

| |

|

2014

|

|

|

2013

|

|

|

2012

|

|

|

2011

|

|

|

2010

|

|

|

Selected Income Statement Data

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net sales

|

|

$ |

58,045,292 |

|

|

$ |

53,353,080 |

|

|

$ |

37,473,966 |

|

|

$ |

35,192,532 |

|

|

$ |

24,366,755 |

|

|

Gross profit

|

|

|

24,598,766 |

|

|

|

21,989,578 |

|

|

|

15,285,721 |

|

|

|

14,658,358 |

|

|

|

9,137,533 |

|

|

Income from operations

|

|

|

8,518,126 |

|

|

|

7,444,735 |

|

|

|

4,274,881 |

|

|

|

3,716,209 |

|

|

|

1,123,412 |

|

|

Income tax expense (benefit)

|

|

|

3,180,978 |

|

|

|

2,803,172 |

|

|

|

(3,324,299 |

)* |

|

|

(2,316,142 |

)* |

|

|

121,458 |

|

|

Net income

|

|

|

5,432,851 |

|

|

|

4,733,844 |

|

|

|

7,701,194 |

|

|

|

6,167,446 |

|

|

|

1,180,954 |

|

|

Net income per share basic

|

|

$ |

0.42 |

|

|

$ |

0.38 |

|

|

$ |

0.62 |

|

|

$ |

0.51 |

|

|

$ |

0.10 |

|

|

Net income per share diluted

|

|

$ |

0.40 |

|

|

$ |

0.36 |

|

|

$ |

0.60 |

|

|

$ |

0.48 |

|

|

$ |

0.09 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selected Balance Sheet Data

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets

|

|

$ |

51,847,898 |

|

|

$ |

46,413,339 |

|

|

$ |

37,740,338 |

|

|

$ |

30,302,091 |

|

|

$ |

21,360,961 |

|

|

Long-term liabilities

|

|

|

- |

|

|

|

21,101 |

|

|

|

37,643 |

|

|

|

61,794 |

|

|

|

78,585 |

|

|

Shareholders’ equity

|

|

|

46,746,634 |

|

|

|

40,078,036 |

|

|

|

34,685,901 |

|

|

|

26,229,171 |

|

|

|

19,246,067 |

|

*During the fourth quarter of fiscal years 2012 and 2011, the Company reversed a substantial portion of a valuation allowance of the deferred tax assets in the amount of $3,518,000 and $2,481,000, respectively. These reversals increased our net income by that amount for each of the years ended September 30, 2012 and 2011 and contributed $0.28 and $0.19 per diluted share for the years, respectively.

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

Cautionary Statement Regarding Forward-Looking Information

Statements made in this Annual Report on Form 10-K, in the Company’s other SEC filings, in press releases and in oral statements, that are not statements of historical fact are “forward-looking statements.” Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results or performance of the Company to be materially different from the results or performance expressed or implied by such forward-looking statements. The words “believes,” “expects,” “anticipates,” “seeks” and similar expressions identify forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date the statement was made. The risks and uncertainties that could cause actual results to differ materially and adversely from those expressed or implied by the forward-looking statements include those risks described in Part I, Item 1A “Risk Factors.”

Overview of Business: The Company sells highly configurable fiber management and connectivity products to broadband service providers serving the FTTP, FTTB, FTT-Cell site markets in the U.S. and in certain limited markets outside the U.S., currently countries in the Caribbean, Central America and South America. The Company’s sales channels include direct to customer, through distribution partners, and to original equipment suppliers who private label its products. The Company’s products are sold by its sales employees and independent sales representatives.

Critical Accounting Policies: In preparing our financial statements, we make estimates, assumptions and judgments that can have a significant impact on our sales, income or loss from operations and net income or loss, as well as on the value of certain assets and liabilities on our balance sheet. We believe that there are several accounting policies that are critical to an understanding of our historical and future performance, as these policies affect the reported amounts of sales, expenses and significant estimates and judgments applied by management. While there are a number of accounting policies, methods and estimates affecting our financial statements, areas that are particularly significant include:

|

·

|

Accounting for income taxes;

|

|

·

|

Valuation and evaluating impairment of long-lived assets and goodwill; and

|

|

·

|

Valuation of inventory.

|

Revenue Recognition Revenue is recognized when persuasive evidence of an arrangement exists, the product has been delivered, the fee is fixed, acceptance by the customer is reasonably certain and collection is reasonably assured. This generally occurs upon shipment of product to the customer. Sales of the Company’s products are subject to limited warranty obligations that are included in the Company’s terms and conditions. Also, the Company offers limited discounts and rebates to customers which are recorded in net sales on an estimated basis as the sales are recognized. The Company records freight revenues billed to customers as sales and the related shipping and handling cost in cost of sales. Taxes collected from customers and remitted to governmental authorities are presented on a net basis.

Income Taxes We account for income taxes in accordance with Accounting Standards Codification (“ASC”) 740, Income Taxes, under which deferred income taxes are recognized based on the estimated future tax effects of differences between the financial statement and tax bases of assets and liabilities given the provisions of enacted tax laws. Deferred income tax provisions and benefits are based on changes to the assets or liabilities from year to year. In providing for deferred taxes, we consider tax regulations of the jurisdictions in which we operate, estimates of future taxable income, and available tax planning strategies. If tax regulations, operating results, or the ability to implement tax-planning strategies vary, adjustments to the carrying value of deferred tax assets and liabilities may be required. A valuation allowance is recorded when it is more likely than not that a deferred tax asset will not be realized. The recorded valuation allowance is based on significant estimates and judgments and if the facts and circumstances change the valuation allowance could materially change.

In accounting for uncertainty in income taxes, we recognize the financial statement benefit of a tax position only after determining that the relevant tax authority would more likely than not sustain the position following an audit. For tax positions meeting the more likely than not threshold, the amount recognized in the financial statements is the largest benefit that has a greater than 50 percent likelihood of being realized upon ultimate settlement with the relevant tax authority. The Company recognizes interest and penalties accrued on any unrecognized tax benefits as a component of income tax expense.

As of September 30, 2014, the Company had U.S. federal and state net operating loss (NOL) carry-forwards of approximately $8,686,000 and $16,641,000, respectively. The U.S. federal NOL carry forward amounts expire in fiscal years 2023 through 2028 if not utilized. The state NOL carry forward amounts expire in fiscal years 2015 through 2022 if not utilized. In fiscal year 2009, the Company completed an Internal Revenue Code Section 382 analysis of the loss carry-forwards and determined that all of the Company’s loss carry-forwards were utilizable and not restricted under Section 382. The Company has not updated its Section 382 analysis subsequent to 2009 and does not believe there have been any events subsequent to 2009 that would impact the analysis.

As part of the process of preparing our financial statements, we are required to estimate our income tax liability in each of the jurisdictions in which we do business. This process involves estimating our actual current tax expense together with assessing temporary differences resulting from differing treatment of items for tax and accounting purposes. These differences result in deferred tax assets and liabilities. We must then assess the likelihood that these deferred tax assets will be recovered from future taxable income and, to the extent we believe that recovery is not more likely than not or unknown, we must establish a valuation allowance. If the valuation allowance is reduced, the Company would record an income tax benefit in the period in which that determination is made. If the valuation allowance is increased, the Company would record additional income tax expense.

During the fourth quarter of 2012, the Company reversed a portion of its remaining valuation allowance in consideration of all available positive and negative evidence, including our historical operating results, current financial condition, and potential future taxable income. The reduction in the valuation allowance in the fourth quarter of fiscal year 2012 resulted in a non-cash income tax benefit of $3,518,000. As a result, we recorded an income tax benefit of $3,324,000 for the year ended September 30, 2012 compared to income tax expense of $2,803,000 and $3,181,000 for the years ended September 30, 2013 and 2014, respectively.

As of September 30, 2013, the Company’s only remaining valuation allowance of approximately $975,000 related to state net operating loss carry forwards. During the fourth quarter of 2014, the Company reversed a portion of its remaining valuation allowance primarily related to the expiration of state net operating losses. The remaining valuation allowance balance as of September 30, 2014 of $848,000 relates entirely to state net operating loss carry forwards we do not expect to utilize. The Company will continue to assess the assumptions used to determine the amount of our valuation allowance and may adjust the valuation allowance in future periods based on changes in assumptions of estimated future income and other factors.

The Company files income tax returns in the U.S. Federal jurisdiction, and various state jurisdictions. Based on its evaluation, the Company has concluded that it has no significant unrecognized tax benefits. With limited exceptions, the Company is no longer subject to U.S. federal and state income tax examinations for fiscal years ending prior to 1999. We are generally subject to U.S. federal and state tax examinations for all tax years since 1999 due to our net operating loss carryforwards and the utilization of the carryforwards in years still open under statute. In 2007, the Company changed its fiscal year from March 31 to September 30.

Impairment of Long-Lived Assets and Goodwill The Company’s long-lived assets at September 30, 2014 consisted of property, plant and equipment, patents and goodwill. The Company reviews the carrying amount of its property, plant and equipment and patents if events or changes in circumstances indicate that the carrying amount of the assets may not be recoverable. When this review indicates the carrying amount of an asset or asset group exceeds the sum of the future undiscounted cash flows expected to be generated by the assets, the Company recognizes an asset impairment charge against operations for the amount by which the carrying amount of the impaired asset exceeds its fair value.

Determining fair values of property, plant and equipment and patents using a discounted cash flow method involves significant judgment and requires the Company to make significant estimates and assumptions, including long-term projections of cash flows, market conditions and appropriate discount rates. Judgments are based on historical experience, current market trends, consultations with external valuation specialists and other information. If facts and circumstances change, the use of different estimates and assumptions could result in a materially different outcome. The Company generally develops these forecasts based on recent sales data for existing products, planned timing of new product launches, and estimated expansion of the FTTP market.

The Company operates as one reporting unit and reviews the carrying amount of goodwill annually in the fourth quarter of each fiscal year and more frequently if events or changes in circumstances indicate that the carrying amount of the assets may not be recoverable. The Company determines its fair value for goodwill impairment testing purposes by calculating its market capitalization and comparing that to the Company’s carrying value. The Company’s goodwill impairment test for the years ended September 30, 2014, 2013 and 2012 resulted in excess fair value over carrying value and therefore, no adjustments were made to goodwill. During the year ended September 30, 2014, there were no triggering events that indicated goodwill could be impaired.

A significant reduction in our market capitalization or in the carrying amount of net assets of a reporting unit could result in an impairment charge. If the carrying amount of a reporting unit exceeds its fair value, the Company would measure the possible goodwill impairment loss based on an allocation of the estimate of fair value of the reporting unit to all of the underlying assets and liabilities of the reporting unit, including any previously unrecognized intangible assets. The excess of the fair value of a reporting unit over the amounts assigned to its assets and liabilities is the implied fair value of goodwill. An impairment loss is recognized to the extent that a reporting unit's recorded goodwill exceeds the implied fair value of goodwill. An impairment loss would be based on significant estimates and judgments, and if the facts and circumstances change, a potential impairment could have a material impact on the Company’s financial statements.

No impairment of long-lived assets or goodwill has occurred during the years ended September 30, 2014, 2013 or 2012, respectively.

Valuation of Inventory The Company maintains a material amount of inventory to support its manufacturing operations and customer demand. This inventory is stated at the lower of cost or market. On a regular basis, the Company reviews its inventory and identifies that which is excess, slow moving and obsolete by considering factors such as inventory levels, expected product life and forecasted sales demand. Any identified excess, slow moving and obsolete inventory is written down to its market value through a charge to cost of sales. It is possible that additional inventory write-down charges may be required in the future if there is a significant decline in demand for the Company’s products and the Company does not adjust its manufacturing production accordingly.

Results of Operations

Year ended September 30, 2014 compared to year ended September 30, 2013

Net sales for the fiscal year 2014 increased 9% to $58,045,000 from net sales of $53,353,000 in 2013. Sales growth was experienced from existing clients as well as from the development of new accounts within the telecommunications industry. The growth in sales includes gains from within Tier 3 Carriers, an emerging presence associated with Tier 2 Carriers who have a national footprint, cable providers as well as non-traditional providers who are entering the U.S. market. The Company also recorded a growing percentage of its sales from accounts outside of the U.S., principally Canada and the Caribbean regions of Central America.

As a result of the above factors, sales in fiscal year 2014 to commercial data networks and broadband service providers were 92% of net sales, or $53,627,000, compared to $48,048,000, or 90%, of net sales in fiscal 2013. Among this group, the Company recorded $5,358,000 in international sales in fiscal year 2014 versus $2,995,000 in fiscal year 2013. Sales associated with build-to-print manufacturing for original equipment manufacturers outside of the telecommunications market in 2014 were 8% of net sales, or $4,418,000, compared to $5,305,000, or 10%, of net sales in fiscal year 2013. The Company allocates sales from external customers to geographic areas based on the location to which the product is transported. Accordingly, international sales represented 9% and 6% of net sales for the years ended September 30, 2014 and 2013, respectively.

The increase in net sales for the year ended September 30, 2014 of $4,692,000 compared to fiscal year 2013 is primarily attributable to an increase of $2,363,000 in international sales. Additionally, the Company’s net sales to our customer base of commercial data network providers, build-to-print and OEM manufacturers, and broadband service providers, outside of internationally noted above, increased $2,329,000 for the year ended September 30, 2014 mainly due to higher demand in fiscal year 2014 when compared to fiscal year 2013. The Company does not have the ability to forecast future sales as revenue from all customers is obtained from purchase orders submitted from time to time. Accordingly, the Company’s ability to predict orders in future periods or trends affecting orders in future periods is limited.

Cost of sales for the fiscal year 2014 was $33,447,000, an increase of $2,083,000, or 7% from the $31,364,000 in fiscal year 2013. Gross margin was 42.4% in fiscal year 2014, as compared to 41.2% for fiscal year 2013. Gross profit increased 12%, or $2,609,000, from $21,990,000 for fiscal year 2013 to $24,599,000 for fiscal year 2014. The year-over-year increase in cost of sales and gross profit is a result of increased net sales. The increase in gross profit percentage is the result of a higher percentage of sales associated with optical component technologies, which generally have higher margins.